In early 2019, I opened the door to my first home.

All the money I had saved my entire life was cleared out at once. I also took out a mortgage. My assets were completely reset. And with the remaining liquidity, I started investing in U.S. dividend growth stocks.

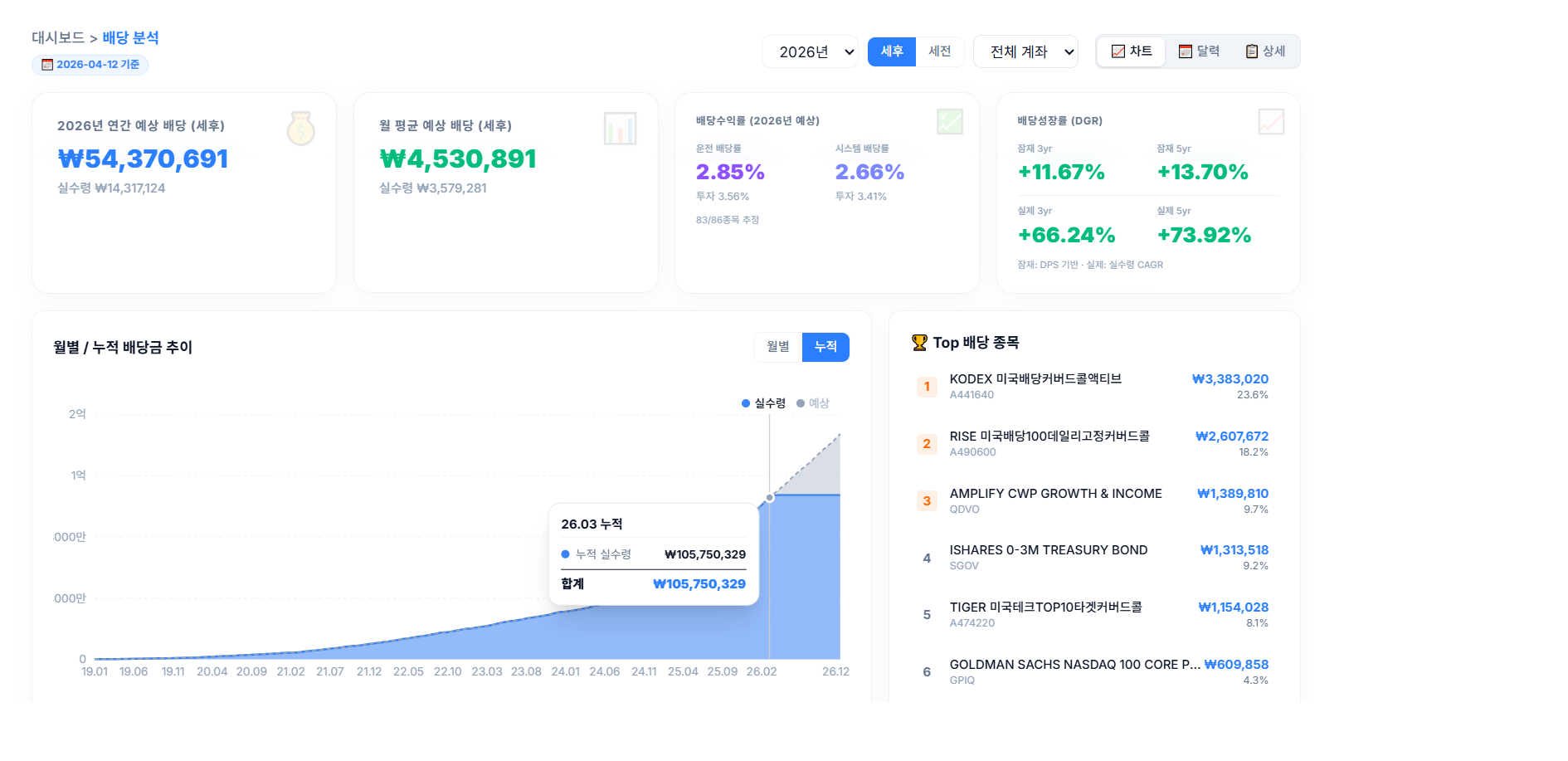

Seven years have passed since then. Today, I receive about $3,100 in dividends every month.

Here, I record the reasons behind that choice.

I Was Playing the Wrong Game

In 2007, I opened my first brokerage account after hearing a friend was making some pocket money through mutual funds. It was an insignificant amount, barely enough to be called seed money.

I started investing in earnest after getting a job in the late 2000s. Individual stocks, KOSPI 200 ETFs. I studied in my own way. However, even after nearly 10 years, there were no meaningful returns.

I was just an ordinary retail investor. I wasn’t a professional trader, nor an institution. I couldn’t watch the market during trading hours. Good news and bad news don’t arrive precisely when I’m sitting in front of my monitor. No matter how much I studied, the result was the same. In a structure where I had to focus on my main job, I simply couldn’t possess the same level of information and response speed as the pros. It was the inherent limitation of an ordinary retail investor lacking both the time and focus needed to generate meaningful returns.

It took me way too long to admit that fact.

20 Failed New Home Lotteries, and the Ceiling of Earned Income

All the while, I kept entering lotteries for new-build apartments. Over 20 times. I failed every single one of them.

At a certain point, I intuitively realized it: No matter how hard I worked, my salary increases alone could never keep up with the soaring speed of housing prices. This wasn’t a matter of effort. It was a structural problem.

In early 2017, I decided not to wait any longer. The real estate market was starting to stir again after a long slump, and the ‘Jeonse’ (key money deposit) that hiked every two years was becoming unmanageable. I couldn’t bet on subscriptions anymore. I paid a premium and bought a pre-sale housing right. It wasn’t the most popular area, but it was close to work and decent for actual living. Looking back now, that was the beginning of the uptrend. The timing wasn’t bad at all. In early 2019, I finally moved into that house.

But by then, I already knew: Real estate ties up a massive amount of capital. Even if its price goes up, no actual cash comes in unless you sell it. True freedom lies in the cash flow that hits your bank account every month. That philosophy solidified from then on. I needed another pipeline.

YOLO Was Not My Answer

In the mid-2010s, ‘YOLO’ became a massive trend. The overarching vibe was to spend and enjoy the fleeting present moment.

While I thought it made sense on some level, it didn’t align with my personality. I couldn’t feel comfortable with a lifestyle that didn’t prepare for the future.

Later, I came across the concept of FIRE: Financial Independence, Retire Early.

I had consistently studied personal finance after getting my job, and the concepts of passive income and multiple income pipelines were already settled in my mind. FIRE was exactly the moment all those pieces fell into place.

When that system covers living expenses, work becomes a choice, not an obligation.

Why Dividend Growth Stocks?

There were many ways to build a pipeline.

I gave up on real estate monthly rent early on. It requires constant management, and liquidity gets stubbornly tied up. Dealing with tenants was another form of stress in itself. I concluded that it was practically too difficult to manage alongside a full-time job.

I also considered high-yield dividend stocks. Tickers with 7-8% yields. The numbers certainly look attractive at first glance. But a high yield doesn’t mean it’s a good investment. If the dividend doesn’t grow, your real purchasing power gets eroded every year by inflation.

Dividend growth stocks were different. These are companies that consistently increase their dividend payouts every single year. Even if the current yield seems low now, in 10 years, the yield on cost (YOC) becomes a completely different number. An annual dividend hike essentially means my return goes up even if I just sit still.

Above all, this system works flawlessly without me having to watch the market during trading hours. This was the most crucial condition for a full-time office worker.

Dividend growth stocks also hold another significant advantage. Companies that consistently grow their earnings to increase dividends tend to experience stock price appreciation in the long run as well. As cash flow increases, the asset value follows a trajectory not vastly different from pure growth stocks. It means you can aim for both robust dividends and massive capital gains simultaneously.

Cash Flow Is Freedom

How much total assets you have is indeed important, but what determines your practical freedom is how much cash hits your account every month. Even if you own a multi-million-dollar apartment, you can’t survive securely without liquid cash. Conversely, if you have a fixed monthly cash flow, your range of choices widens tremendously, regardless of your ultimate asset size.

At first, I aimed for approx. $3,000 a month. Later, as my family situation evolved, I raised the goal to $3,500~ $4,000.

The current structure of my pipeline looks like this:

- Dividends: approx. $3,000

- Additional Pipeline: approx. $500 ~ $700

I have continuously experimented with various methods for generating income outside of dividends. One of them is FX futures. As my dividend income grew, the burden of comprehensive financial taxation and health insurance premiums increased steadily, so I began a system leveraging FX gains. The returns have proven to be more stable than initially expected. I am still continuing my experiments to diversify income pipelines far beyond mere dividends.

The Results Over 7 Years

I started this journey in earnest in 2019. My initial timeframe was 10 years.

But the progression was much faster than I anticipated. As dividends increased, the speed of compound reinvestment accelerated dramatically. You buy stocks with pure dividends, and those very same stocks generate more dividends. It was a literal snowball effect. By my 7th year, I had practically reached my original goal.

The total asset value of the portfolio itself has also steadily appreciated over the long term. Cash flow grew robustly, and the underlying assets grew effectively right alongside it.

But what changed isn’t strictly the numbers. It’s the fact that I now possess choices. That is everything.

I Decided to Document It

As my dividends grew, so did the sheer volume of data I had to strictly manage.

Dividend growth rates, exchange rate adjustments, portfolio weightings by ticker, monthly historic trends. I managed all this in Excel until I inevitably hit a wall. So, I built my own bespoke dashboard. It is a robust tool designed to analyze and continuously monitor my portfolio in real time.

I am actively documenting that exact process, the resulting data, and my thoughts accumulated over these 7 years right here on this blog.

There are no grandiose or unrealistic goals. It’s simply the honest record of one person systematically pursuing FIRE through dividend growth investing. Whether this exact strategy is right or wrong, the raw data will ultimately tell.