It’s been a few years since I started steadily building up my dividend income. Early this year, my post-tax monthly cash flow finally crossed 4.5 million KRW. Considering I initially thought, “If I hit 5 million KRW a month, I can achieve FIRE,” I should feel like I’m almost there.

But something was strange. As the numbers got closer, the final decision actually became harder. I couldn’t find the conviction to say, “I can quit right now.”

After a long thought, I found the root of the problem. Tracking FIRE spending — knowing exactly how much I actually spend in a month — I had never done this properly. I had spent years running towards a goal without verifying if my initial estimate of “about 4 to 5 million KRW a month” was actually accurate.

💡 Plan B Insight: The Core of This Post

When preparing for FIRE, people usually focus on asset size or cash flow targets. But there is a question you must answer first. Exactly how much is my monthly spending? If you don’t know this, you won’t feel confident even when you hit your target. This series records the discoveries I made while trying to track my spending accurately.

1. Why Tracking Spending is the First Step of FIRE Preparation

Most people set their FIRE goal as “Accumulating X amount of assets.” Is 1 billion KRW enough, or does it have to be 2 billion? But an asset target is actually a reverse calculation. First, you need to know how much you need per month to reverse-engineer the required asset size or target yield.

The sequence should be:

Identify monthly spending → Calculate required monthly cash flow → Reverse-calculate target assets → Establish investment strategy

The very first and most important step in this sequence is tracking spending, but many people just gloss over it. I did too.

2. Initially, I Just Guessed with Excel

When I first seriously considered FIRE, I opened an Excel sheet. I listed out my fixed expenses: loan interest, phone bills, insurance, apartment maintenance fees… And for living expenses, I typed in “about 2 million KRW?” The total came out to around 4.3 million KRW. “Alright, 5 million KRW a month gives me some breathing room.” Just like that, the goal was set.

The problem only revealed itself a few years later.

📌 Why Excel estimates miss the mark

There are items that naturally slip your mind. Quarterly insurance premiums, annual car taxes, congratulatory/condolence money, sudden medical bills. Because these don’t appear clearly on your monthly credit card statements, they are treated as non-existent money during estimation.

When I got close to my goal, something weird happened. I hit the number, but couldn’t make the decision. The doubt of “Is this number really accurate?” wouldn’t go away. I realized then that a goal built on inaccurate data leaves you anxious even after you achieve it.

3. Spending Data is Scattered Everywhere

You might say, “Well, just tally it up properly then.” But when you actually try to do it, you hit a wall. The data is too fragmented.

Multiple banking apps, multiple credit card apps, and brokerage apps, all separate. MyData services emerged, but the structure of having to check each institution individually hasn’t changed much. Past data is usually only available for the last 1 year online. To get history before that, you have to call the credit card company and go through a separate request process.

Ultimately, your spending remains in a state of “I think I know, but I don’t know exactly.” In this state, you simply cannot make the FIRE decision.

4. Monthly Credit Card Bills Create Optical Illusions

Even if you gather all your spending data, treating “this month’s credit card bill” as your actual monthly spending is a trap.

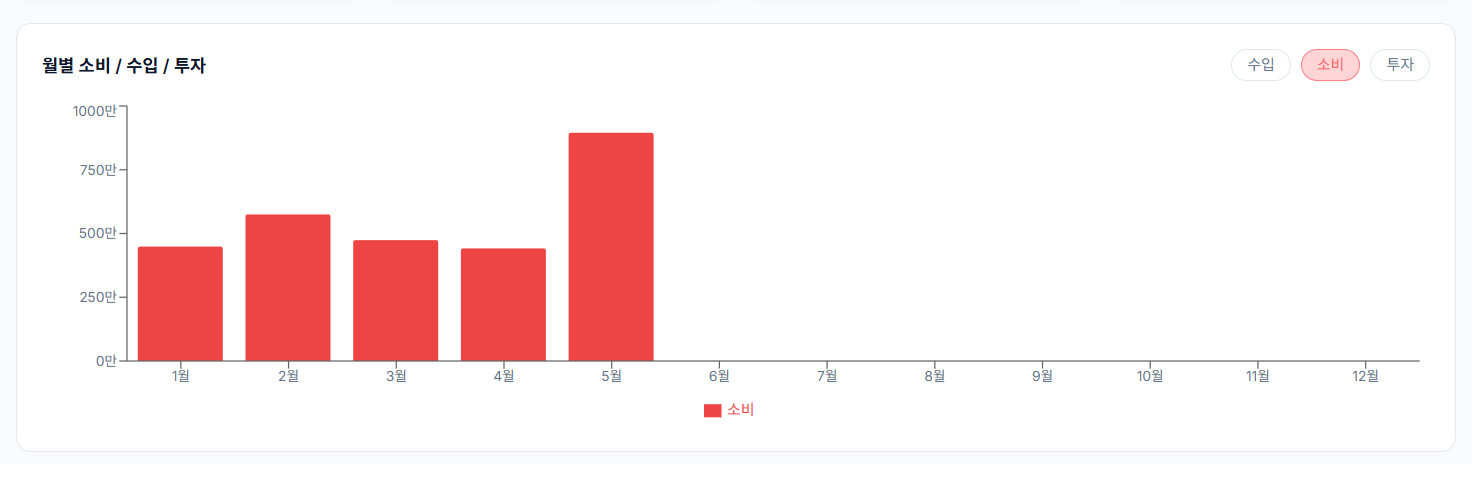

This May was exactly that kind of month.

| Month | Spending Amount | Note |

|---|---|---|

| Jan | 4.48M KRW | |

| Feb | 5.74M KRW | Included Lunar New Year |

| Mar | 4.73M KRW | |

| Apr | 4.41M KRW | |

| May | 8.97M KRW | Additional Comprehensive Income Tax & US Stock Capital Gains Tax |

| Monthly Required (Tax Annualized) | 5.19M KRW | Taxes distributed over 12 months |

It is true I spent 8.97 million KRW in May. But this month included an additional comprehensive income tax payment and US stock capital gains tax. These taxes are fixed annual expenses, but they all concentrated in May. If I conclude “My monthly spending is 8.97M KRW” based on this, the number gets completely distorted.

To establish a practical baseline for monthly spending, you must distinguish between 3 types of expenses: Fixed (same every month), Variable (fluctuates), and Irregular (concentrated in specific months). Expenses like taxes, which are annual but concentrated in May, look like an anomaly if you only look at that month, but when divided by 12, they are just part of your fixed monthly expenses.

INSIGHT It’s not 8.97M KRW, it’s 5.19M KRW

May’s spending of 8.97M KRW and the required monthly amount of 5.19M KRW are data from the same person in the same month. Depending on how you read it, the judgment on whether FIRE is possible completely changes. You must first decide on a methodology for handling irregular expenses to find your true FIRE baseline.

5. Post-FIRE Spending Will Be Different

There is one more reason you must track your spending. To predict post-FIRE spending, you must know the itemized structure of your current spending.

When you quit your job, commuting and lunch costs will drop. On the other hand, spending on leisure, travel, and health is highly likely to increase. To predict this change, you need to know exactly how much of your current transportation cost is “commuting” and how much of your dining out is “business lunches”.

| Category | Now | Expected Post-FIRE |

|---|---|---|

| Transportation/Gas | Includes commuting | Expected to decrease |

| Dining/Lunch | Includes work lunches | Expected to decrease |

| Leisure/Travel | Mostly weekends | Expected to increase |

| Health/Medical | Minimal | Expected to increase |

| Child Education | Current level | Expected to increase |

Without data, you’re back to relying on gut feeling.

⚠️ This post shares personal financial management experiences and does not recommend specific investments or financial decisions. Please make judgments fitting your situation or consult an expert.

Series — Designing the Flow of Money

Part 1 · Current Post

Why Receiving 4.5M KRW a Month in Dividends Still Makes FIRE Scary

Part 2

How a Single Receipt Automatically Becomes a Ledger

Part 3

May Ledger Revealed: I Spent 8.97M KRW

Part 4

Where Does My FIRE Journey Stand Right Now?